Exception-based workflows

Performance attribution is a complex area. Most of the complexity lies in ensuring data needed is accurate and complete.

Transaction-based performance calculations are the next obstacle to overcome. Once there however, the actual performance numbers are surprisingly simple to calculate.

This article looks at the different solutions to getting the data requirements right. We then go into ways to calculate performance and approaches to migrating to a new system.

Investment performance reporting

Once you have the performance numbers, you need ways to report them. Display of data within the application is available in all performance systems we know. Many enable you to export the data to CSV/Excel files.

Limina takes reporting one step further, by having reporting software as an integrated component of the product suite. With the investment performance reporting software, you can create your own reports, integrate with BI platforms and there’s even a native Excel plug-in.

Standalone system vs integrated

Standalone system vs integrated

The accounting book of record usually isn’t adequate to be the basis for performance calculations. Treatment of accrued income and dividends, is posted to accrual accounts and not included in the P&L calculation of the holding. Which doesn’t work for performance calculations.

If you have a 2nd or 3rd generation investment book of record such as Limina, that data source is already prepared for calculating performance. All transactions and cash movements are already in the system, data quality has been checked, and P&L is calculated on a position basis.

Since Limina is a portfolio management system, it’s also used for portfolio rebalancing. For this application, benchmarks are used – either to rebalance against or to see how exposures compare to benchmarks when rebalancing. In other words, the benchmark data is already in the system!

With all the data already available and quality controlled, attribution is just a matter of calculations. No additional work is required by your team - no integrations, etc. Performance attribution reports are produced at the click of a button. Book a no-strings-attached demo of Limina to see it for yourself.

Migrating from existing portfolio attribution software

If you have a performance attribution tool in place and are considering changing to another one, you will probably want to bring historical data. There are two ways to do this:

| Approach | Pros | Cons |

| Move all underlying data (steps 1-2 above) and rerun calculations in the new attribution software | Gives you the flexibility to change attribution model historically | Very time-consuming to replicate historical TWR calculations |

| Move only the calculated performance numbers | Fast to implement and low risk (using already validated numbers) | Might not be well-supported by all systems (Note: this is supported in Limina) |

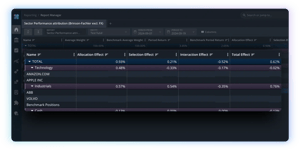

Limina’s Performance Attribution System

Limina’s investment performance software is part of our investment management software suite. Data quality controls are centralised and a book of record engine can produce portfolio views for any use case – including performance. All modules leverage the data controls that are performed once, so you don’t have to maintain data in various places.

The calculations are transaction-based daily TWR (the most accurate approach) and history can easily be migrated. Finally, calculations are inspectable, so you have full transparency into how a number has been derived with the click of a button.