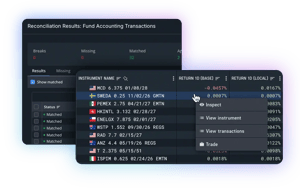

Exception-based workflows

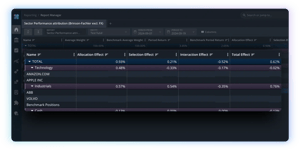

Performance measurement & attribution

View, analyze and report your portfolio returns compared to benchmark.

An easy way to explain your investment returns

Our flexible performance attribution helps you easily analyze and explain the drivers of excess return vs. benchmark.

Using market standard attribution models (Brinson-Fachler - incl./excl. FX), you can analyze returns on sector, geography or any other custom segment - across any time period.

Accurate & transparent

No approximations - our performance attribution is based on your actual daily data:

- Transaction-based (using the reconciled transaction data in Limina)

- Includes all fees and expenses that contribute to the NAV

- Returns calculated as daily time-weighted returns (TWR), ensuring accurate representation of inflows/outflows

- No black box - inspect figures to see how they are calculated

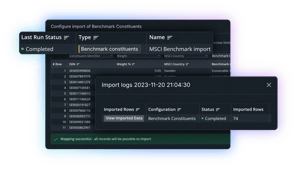

Out of the box

No integration pains.

Integrating external performance attribution software can be challenging, due to the scope and complexity of the data involved.

Not with Limina, since our performance attribution functionality leverages the quality-controlled data in Limina directly.

FURTHER READING

Limina IMS - Functional coverage

TOUCH

TOUCH

TOUCH

Investment Compliance

Pre- & Post-trade Compliance, smoothly embedded in the investment lifecycle.Read More

TOUCH

TOUCH

TOUCH

Investment Operations

Trade affirmation, reconciliation, position lifecycle events and more.Read More

TOUCH

TOUCH