Exception-based workflows

This article aims to uncover why there are so many different Books of Record (BOR) in Asset Management. The definitions of Investment Book of Record (IBOR), Accounting Book of Record (ABOR), Performance Book of Record (PBOR) and Custody Book of Record (CBOR) isn’t always obvious. We also dig into what problems this causes and how to reduce the number of BORs.

Can there be multiple Books of Record (BORs)?

A Book of Record in Asset Management is defined as all records that make up a portfolio. It is, by implication, the truth. But, there are multiple books of record deployed in asset management and they surely can’t all be the truth?

We hear about multiple books of record in asset management because, quite legitimately, different business areas demand different perspectives on positions and transactions. These demands are met, conventionally, by maintaining different books of record for different purposes.

Our founder and CEO, Kristoffer Fürst, takes you through a full IBOR breakdown in the video above

How it all started: Accounting Book of Record (ABOR)

Historically, the first automation built specifically for investments was in the form of accounting systems, which delivered an Accounting Book of Record. These naturally took a view of the world that reflected the relevant accounting practices. And so, an accounting perspective was the starting point.

For business areas with other needs, the front office, for example, had to either

- Make the best of the accounting positions; or

- Manipulate and augment them to suit their own requirements

Over time, this dependency on an ABOR became burdensome and risky. Despite ABOR and IBOR reconciliation, data inconsistencies between ABOR vs IBOR could arise. As one example, a dividend either being overlooked or not adjusted in the cash trade-date view of the Front Office.

The main difference between IBOR and ABOR is that the Front Office requires portfolio data to be constantly available, which is not a requirement in accounting. ABOR system design didn’t prioritise data availability and on-time delivery.

As such, the need arose for books of record available on demand and specifically tailored to the needs of the investment team, the performance team, the control and recons team, the investment accountants, etc.

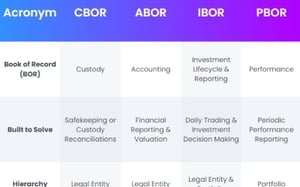

The four most common Book of Records (BORs): ABOR vs IBOR vs PBOR vs CBOR

The most common BORs are:

- Investment Book of Record – IBOR

- Accounting Book of Record - ABOR

- Performance Books of Record - PBOR

- Custody Book of Record (not to be confused with Client Book of Record) - CBOR

In this article, we assume that all BORs are cross-asset. In a procurement, however, asset class coverage is something to pay close attention to.

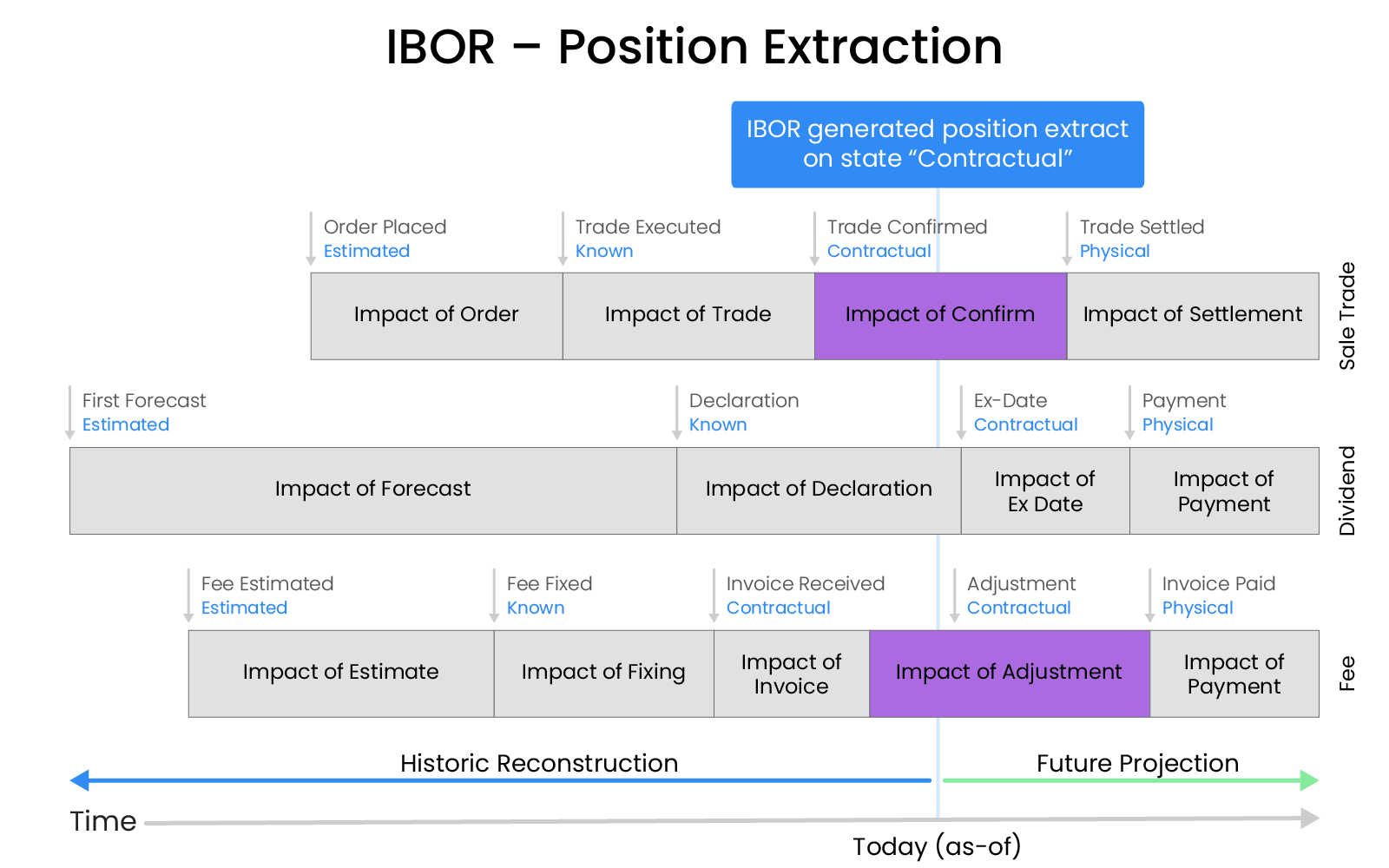

Investment Book of Record (IBOR)

IBORs can have two interpretations:

- Seen narrowly, IBORs are the position and transaction views that investment managers need to support investment decision-making. These views are generally constructed to include orders as well as executions and may accommodate trading intentions and what-ifs also.

- In the broader perspective, they are a single book of record, from which it is possible to extract whatever view is requested by the user or calling process. In this context, IBOR may be better labelled “Universal Book of Record” (UBOR).

Regardless of the interpretation, real-time timely data is a fundamental concern of an IBOR. It’s there to ensure portfolio managers have the information they need when they need it.

ABOR Accounting Book of Record

An ABOR is often referred to as “the books and records of the business” because it is the basis for statutory submissions and is the target for statutory audit. In constructing positions, ABORs (very obviously) include only transactions posted to the accounts. A strong point of accounting records is that they have to be complete – the data an ABOR contain must be all transactions of any kind, or the accounts are wrong. The completeness of accounting records makes them valued either as a source or as a reconciliation check on our books of record.

Accounting standards vary across jurisdictions, but it’s a good generalisation that account postings occur (or should occur) when a transaction turns into a contractual asset or liability. Such postings can be some time after the transaction is known in the front office (and elsewhere). For a standard equity trade, this is when the trade is confirmed between the parties. Before posting to the accounts, the trade is, in effect, invisible from an ABOR perspective, as is a dividend before its ex-date.

IBOR vs ABOR

It’s worth noting that the position level view in an ABOR aggregates transactions into positions on legal entities. ABOR compared to IBOR differ in this matter, since investment functions request a different aggregation, e.g. portfolio or strategy level. Hence, middle offices have a challenging task when reconciling the two.

Performance Book of Record (PBOR)

A Performance Book of Record (PBOR) exists to support performance measurement, both performance attribution and contribution, in absolute terms and against benchmarks.

PBORs are based on trade-date position views, supported by portfolio cash flows (especially injections and withdrawals) and security trades. It is an essential feature of a PBOR that transactions selected in any period are aligned (as far as possible) with update timings of any index used in the performance calculations. Pricing used in valuations needs to be similarly well-aligned with any reference index.

Performance results, whether for client performance reporting or attribution, are conventionally computed from period-end to period-end and based on start or end-of-day positions. They do not have to be, however: it would be quite reasonable, for example, for an investment manager to want to see an attribution report from one rebalance to the next. The rebalances will almost certainly not align with period- or day-ends.

Custody Book of Record (CBOR)

A Custody Book of Record (CBOR) take the custodian’s perspective, which means that settlement is the critical step in the transaction lifecycle, whatever the transaction type. Positions delivered from a CBOR are, therefore, on a settled basis, reflecting the ‘physical’ existence of the delivered asset at the custodian and / or the ‘physical’ presence of the cash at the bank.

The settled view is the most helpful for reconciliations to custodians and bank accounts. It’s used in the back office of asset managers and service providers for that purpose. It’s also crucial in managing physical cash in portfolios and as a starting point for cash positions in treasury systems.

|

Acronym

|

CBOR

|

ABOR

|

IBOR

|

PBOR

|

|

Book of Record (BOR)

|

Custody

|

Accounting

|

Investment Lifecycle & Reporting

|

Performance

|

|

Built to Solve

|

Safekeeping or Custody Reconciliations

|

Financial Reporting & Valuation

|

Daily Trading & Investment Decision Making

|

Periodic Performance Reporting

|

|

Hierarchy

|

Legal Entity

|

Legal Entity

|

Legal Entity & Portfolio

|

Portfolio

|

|

Transaction State

|

Settle Date

|

Posted Date

|

Posted Date & Trade Date

|

Trade Date

|

|

Data

|

Assets

Cash

|

Market Values

Transactions

GL

|

Orders

Executions

Valued Positions

Analytics

Cash

|

Open Positions

Exposure

Returns

|

|

Data Quality

|

Reconciled to Accounting

|

Complete As Posted, Reconciled to Custody

|

Intra-Day, Previous days reconciled to Accounting

|

Reconciled to Accounting

|

|

Reporting Period

|

Periodic / Closed

|

Periodic / Closed

|

Intra-Day / Live

|

Periodic / Open

|

Problems with multiple BORs

Each book of record has position views and underlying transactions that overlap strongly with all the other books of record. These must be maintained, so the more BORs there are, the greater the data management workload becomes.

There must be no inconsistency between the data on which investment decisions are made, the data on the resulting positions, and the data reported to the client. Telling the client a different story from what is known internally is not just unfortunate, it can become a compliance breach or a basis for litigation.

So even though their perspectives differ, it is vital to maintain a relationship between the various books of record exhibiting demonstrable integrity.

Maintaining the various books of record takes data management effort, and ensuring their consistency takes reconciliation effort too. The differing perspectives of the different BORs make the reconciliations more complex, so a straight delta comparison is inadequate.

Reducing the number of Books of Record

A key use case of an investment book of record is to eliminate the parallel maintenance of multiple books of record. Having one internal BOR removes complex reconciliations between the various BORs and replaces them with a single, definitive transaction store. If maintained in a complete, timely, accurate, multi-state and bi-temporal form, this transaction store can support any perspective on positions that a user (or requesting process) may need.

A live-extract book of record can eliminate the need to maintain multiple BORs while delivering to the different needs of diverse business users. It can be wholly independent of accounting and deliver timely position views much earlier than account postings allow in an ABOR. Based on a single underlying data store, it eliminates the need for reconciliations between the resulting position views.

A live extract Position & Cash Management Software (i.e. a true generation 3 IBOR) also supports a much wider and more flexible range of use cases than rigid, single-purpose BORs. So, for example, in the attribution use case above, can provide exactly the data needed to deliver an attribution analysis from one rebalance to the next.

This article was co-authored by Kristoffer Fürst, CEO of Limina, and Doctor Ian Hunt, independent consultant and IBOR expert.

For full disclosure: Part of why we started Limina in 2014 was our recognition of the challenges in trusting and accessing position data. Consequently, Limina’s system is both an Investment Book of Record and an Accounting Book of Record. However, this post hasn't been written as a pitch for our solution, and we hope you've appreciated it and that it has answered questions like "What are IBORs and ABORs?". This article part of our entire series of articles on IBOR Systems which we encourage you to read!